25. 02. 2015.

A fundamental analysis on bitcoin? Something that is completely intangible, and its price is determined by the current strength of a far-fetched belief? The momentary state of mind of eccentrics?

No doubt, trust is an important factor in the context of the price of bitcoin. During the Cyprus banking crisis, as general confidence in the conventional financial system was undermined, bitcoin performed a huge rally because it began to be viewed by many people as an alternative to the monetary system. Then, when the bitcoin exchange MtGox failed, it was bitcoin in which confidence was shattered, as could be traced neatly on its price curve. Changes in sentiment are priced in rather markedly, as further examples could illustrate. Despite that, there is a factor that may be addressed within the conventional framework of economics, which could be dominant when the price is not diverted in either direction by matters of confidence. Taking a closer look at bitcoin mining, we might as well produce some kind of fundamental analysis on the virtual money.

The model

I have recently seen an interesting video on a Chinese bitcoin mining business. It made me want to do some calculations on the returns generated by these mines. Bitcoin mining requires purpose-built hardware to run software, which consumes electricity while it “finds” bitcoins. According to a simplified model that nevertheless adequately describes the essence of the process, there is an initial fixed cost (the price of hardware), a variable cost (the price of the electricity consumed), and revenues are generated in bitcoins.

Hash factory

The funny thing is that it is possible to estimate the quantity of the electricity consumed by the entire bitcoin network. Mining bitcoins requires one thing to be done really well, and that is the ability to compute so-called hashes at great speed. Somewhat simplified, the system works like this: approximately every 10 minutes, 25 bitcoins are raffled between miners, and the chance to win is proportionate to the number of hashes computed. If I was a bitcoin miner, I would have an interest in computing as many hashes as possible. For that reason, gadgets are already produced for miners which can do nothing else but compute hashes at very high speeds. In principle, this could also be done with ordinary computers, but they stand no chance against purpose-built hardware.

The bitcoin network continuously and transparently calibrates itself so that irrespectively of the number of hashes computed by all miners, 25 bitcoins should be generated in every 10 minutes. This allows an estimate to be made for the number of hashes computed by the entire network over a unit of time. Nowadays it is 340,000,000,000,000,000 hashes per second.

The cost of electricity

As we are also familiar with the technical parameters of the gadgets currently in use, we know that they compute 1 to 2 billion hashes using 1 Joule of energy. Based on that, the electric power consumed by the bitcoin network is estimated at 170 to 340 MW. In other words, the world is using an amount of power to mine bitcoins that is equivalent to that produced by one half of a block at the Paks nuclear power plant.

Obviously, most bitcoin mines operate in countries where electricity is cheap. If the price of 1kWh of electricity is assumed to be 10 dollar cent (utility cost reduction or not, in Hungary that comes to about 1.5 times to twice as much), then it is possible to calculate that producing 1 bitcoin requires approximately 150 dollars worth of electricity. Note that it is only the cost of electricity, and given the fact that the price of 1 bitcoin is currently about 240 dollars, mining bitcoins does not appear to be a very good deal. In fact it is not. But it has not always been that way.

Returns on mines

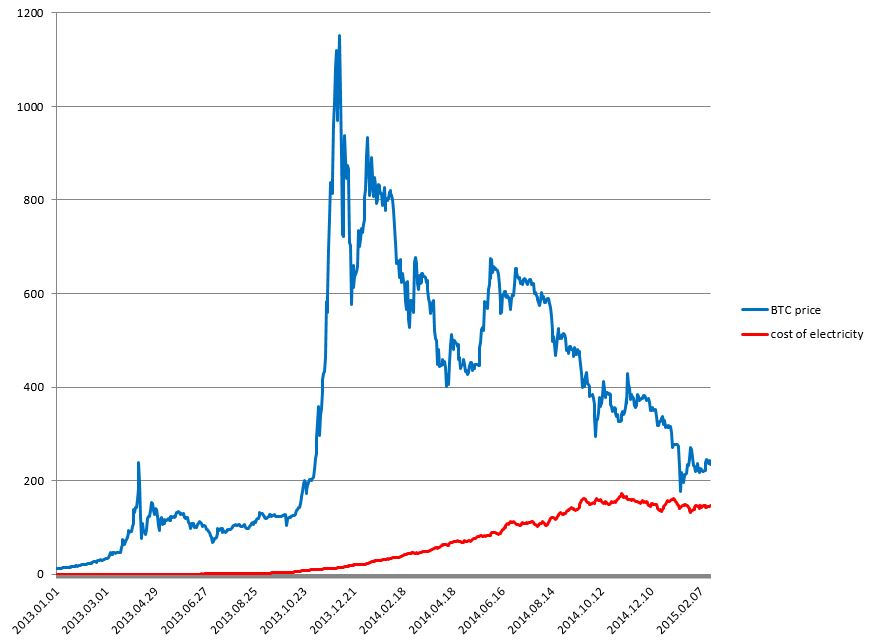

The above data can also be gathered with reference to the past, and although some reasonable assumptions are needed in respect of the energy efficiency of the bitcoin network (I have rummaged for the technical parameters of older mining hardware for that purpose), magnitudes and trends appear to be obvious. The chart shows the price of 1 bitcoin and the cost of electricity required to mine 1 bitcoin over the past 2 years.

How does a typical bitcoin miner think? As the cost of the electricity consumed is covered by the sale of the bitcoins produced, it is worth putting more and more mining hardware into service as long as the proceeds also provide sufficient coverage for the cost of capital. That is to say, in this phase of the life cycle of the bitcoin network, the cost of electricity required to mine 1 bitcoin is increasing dynamically. However, this trend broke last autumn and turned into stagnation as the gap between the two curves narrowed. Currently it is not worth deploying additional mining hardware as it will probably not pay off its price.

Effects

The daily cost of electricity for the entire bitcoin network over time looks exactly the same as the above curve, since bitcoins are generated at a constant rate of 3,600 per day. Namely, until last autumn miners had flushed bitcoins on the market in an increasing value to cover their cost of electricity. In turn, they found buyers at gradually decreasing prices. However, the trend broke a few months ago, and since then the daily electricity cost of the bitcoin network has been level at approximately half a million dollars a day. That is also equivalent to the amount for which new demand, i.e. new bitcoin investors need to be attracted every day. It is a positive development that the value has stopped rising.

Does that also mean that the bitcoin has stopped falling? Not necessarily. What has changed is that a further decline in the price of bitcoin will make it unprofitable for miners producing more expensively to continue their operations, since not even their electricity cost would be paid off. In that case, the red curve will also start descending (it must remain below the blue one), and simultaneously the value of the bitcoins flushed on the market by miners will also start falling. That is, (net) new bitcoin investors will have to be attracted for a gradually diminishing value, which is in turn an effect countering additional falls.

The probability that the deployment of new mining hardware has virtually stopped also works against additional falls. The time will soon be over when miners also want to recover the price of hardware, i.e. their fixed costs from the sale of bitcoins produced. Being in no hurry to market, they will be increasingly keen to keep the mined bitcoins to themselves. Let me point out again that irrespectively of all this, the price may well continue to fall in the absence of adequate demand.

Notes

In the foregoing, I assumed that in a manner suitable to bitcoin fans, miners will also keep some of the virtual money in addition to covering their costs, and will not market all of it. This seems probable—who else would be mining than the greatest bitcoin buffs? They represent natural first-round demand for newly generated bitcoins. In the video referred to above, entrepreneur Jin Xin also claims to keep a half of his assets in bitcoins.

The price of the bitcoin may be greatly influenced by non-recurring effects such as those referred to at the beginning of this article.

Such effects may decelerate both decreases and increases in the price of the bitcoin. If the price moves upwards, additional mining hardware will be deployed and the cost of electricity will increase, and so will the value of the bitcoins which miners are forced to market.

Miners will also receive a voluntary commission on bitcoin transactions, but its value is negligible compared to that of the bitcoins mined.

In two years, the number of bitcoins mined every 10 minutes will drop to 12.5. If this happened tomorrow, a lot of miners would close shop immediately. Consequently, the electricity consumption of the network would drop dramatically, and so would the value of bitcoins marketed under pressure.

If you are considering a bitcoin investment, remember that the price of the bitcoin may also be reduced to zero. Limit your investment to an amount the complete loss of which does not hurt excessively.

Related posts: